The beginning of the year is always time to summarise the results and trends that had the greatest impact on the analysed market sector. Like every year, I could start my summary by saying - it has been a challenging year for the FMCG industry. It will certainly also come as no surprise that the main challenge the industry faced in 2023 was primarily cost increases and the associated price pressure, but this is nothing new for those operating in the retail sector. Additional challenges that we have often talked about in 2023 - which are often a derivative of rising prices - are the growing number of consumers actively seeking savings and adopting various saving strategies, and the demographic changes in society related to migration, digitalisation and the rising minimum wage. It is also worth noting that the challenges faced by the Polish FMCG market are also challenges in global markets - where both inflationary pressures and demographic changes have had a significant impact on the retail market.

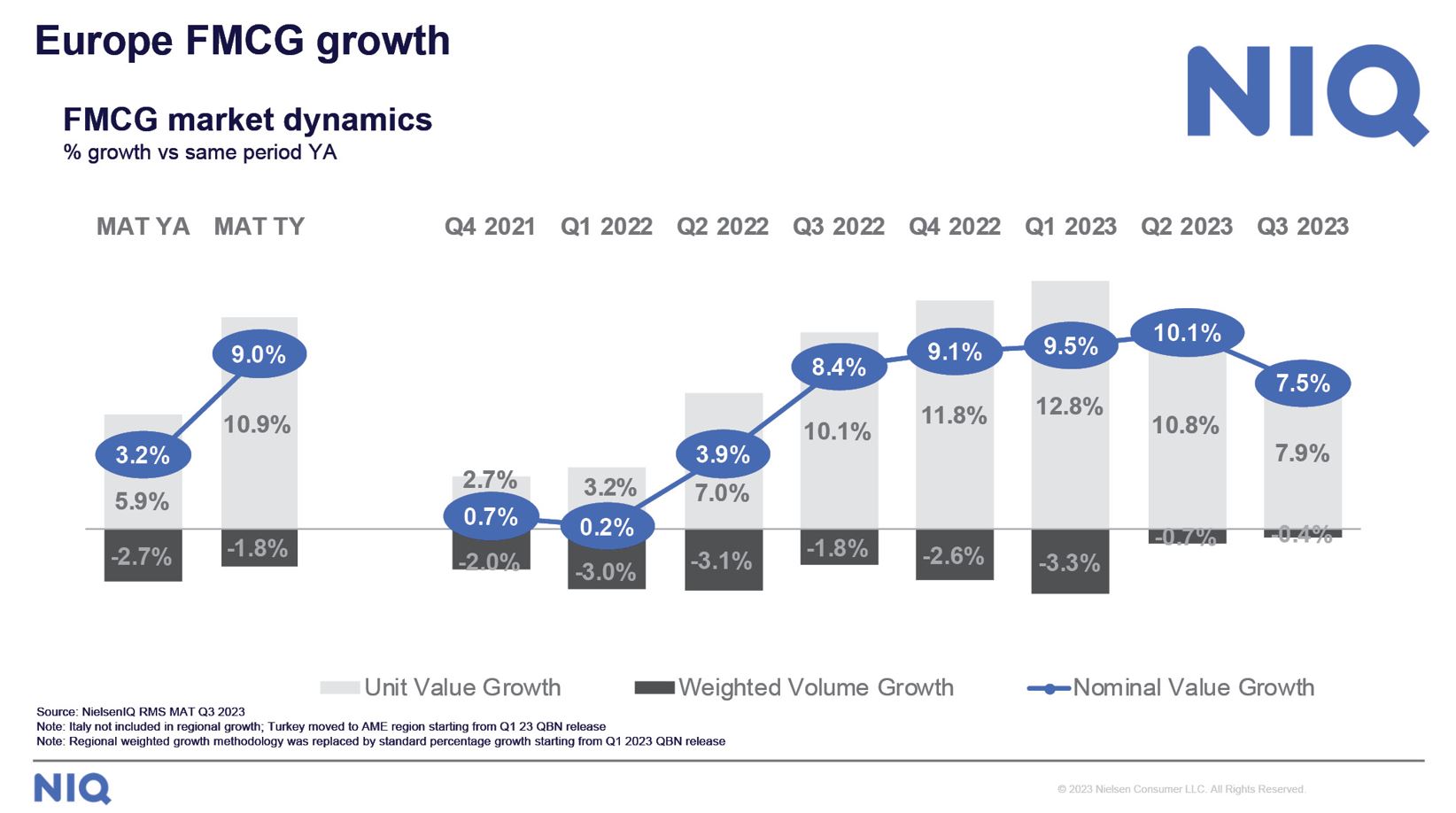

From a global perspective, the FMCG market in 2023 grew by nearly 9% in terms of sales value (analysing the 12 months to the end of September 2023). Market dynamics in Europe also achieved a similar result. In Poland, the FMCG market grew by 11.7% year-on-year in value terms in the last 52 weeks ending 10.12.2023. One can venture the opinion that in the face of all the challenges - this is a positive double-digit market value growth. Unfortunately, looking at the sales volume in the perspective of the Polish FMCG market in 2023, we are rather talking about stagnation or even a slight decline - especially in Q1 and Q2 (which, in the previous year, saw the outbreak of war in Ukraine and a large migration of citizens from Ukraine to Poland).

The year 2023 also saw the continuation of trends already known on the Polish retail market - the strengthening of the position of discount stores, which, taking into account the sum of food, chemical, cosmetic and tobacco products, reached a weight of 38% of the market, recording an increase of over 18% in the value of sales. Supermarkets, drugstore chains and online sales channels also recorded significant sales growth. Taking into account sales from the largest marketplaces - the importance of the online channel in Poland in selected cosmetic categories according to NielsenIQ - e.g. body care or facial care - is already close to 15% of the total market. This confirms that the trend, which has been with us for a long time and has been booming since the pandemic, of some sales categories moving to ecommerce, has already reached a significant level.

Despite a drop in inflation in the second half of the year (to 6.5% in November 2023 according to the Central Statistical Office) - Polish consumers have spent this past year perfecting their savings behaviour. Although grocery shopping decidedly did not appear as the first category on which we want to save - 56% of shoppers said in the September reading that they plan to save on FMCG products (source NIQ Shopper Trends Pulse 2023). This effect was visible in various dimensions - some categories such as alcohol - above all in the largest categories, i.e. beer and vodka, recorded declines in volume sales in 2023. Poles bought less alcohol than a year ago (an unprecedented situation in the last decade). Another area undoubtedly influenced by frugal attitudes is the chains’ private labels. The chains’ private brands-which still, in the opinion of shoppers, have the advantage of being cheaper products-recorded a 20% increase in the value of sales for food products (also supported by a slight increase in volume). The trend of increasingly choosing chain brands is also evident in other regions, globally private labels achieved a growth rate of 13% vs 9% of the entire basket including manufacturer products. Increasingly, we are also seeing dedicated advertising and marketing campaigns targeting specific brands of the chain’s own brands - showing that these brands are often already leaders in their categories. The third common behaviour of shoppers managing their budget was to actively seek out promotions. The share of promotions in the FMCG basket in Poland did not increase compared to the previous year - in the hypermarket and supermarket market, it remained at 33% of value sales made during promotions. However, consumer expectations of promotions are increasing - the importance of an attractive promotional offer is rising in the ranking of factors influencing shop choice. This forces chains and suppliers to pursue a very targeted and effective promotional and pricing policy, often tailored to the location, shopper or current market need.

We are entering 2024 with optimism, bidding a hopeful farewell to double-digit inflation, looking forward to a more stable and predictable political situation and hoping that consumers will slightly loosen the hitherto restrictive attempts to keep their money in their wallets and be able to shop more often on Sundays (if the promises of the current coalition are fulfilled). What can we expect from trends in the FMCG market?

Taking into account the lessons of the 2007-2010 economic crisis, we can expect learned savings mechanisms to remain with Polish consumers even if their economic situation improves in the coming years. This may give rise to several changes in the market - one of which will be a redefinition of price levels and assortment - adjusting the offer to a more polarised society, where an important group of consumers can afford premium products and an equally large group, will look for a more economical offer. The search for promotions and the development of technology has meant that already the vast majority of shoppers are also taking advantage of loyalty or points programmes offered by retail chains. Development in this area will also be an important trend in 2024, bearing in mind the need to control spending and buy products with tailored and attractive offers will also remain with us.

A significant challenge that the FMCG industry will have to deal with in 2024 is also, rightly, the pressure to move towards climate neutrality. The packaging deposit system introduced is just one element related to the industry’s commitments, which will affect a significant proportion of the FMCG sectors. Caring for the planet and being in line with the European Green Deal also ties in with the trend towards health and general wellbeing - which will also be an important market driver in the coming years. In the short term, we will observe the impact of regulations banning the sale of energy drinks to minors, while in the long term, products guaranteeing a proactive approach to health or responding to civilisation-related illnesses have growth potential (we can already see specialist Superharm medical centres appearing on the Polish market or promotional campaigns for health-oriented products undertaken by, for example, Amazon).

The development of the FMCG market in 2024 and beyond must also take into account the demographic changes in society. In 2030, 54% of FMCG spending will be carried out by the 50+ group, which will of course be an active and very aware social group. It will be worth using these remaining few years to develop offers aimed at the ‘silver generation’, and to create technologies and solutions with older consumers in mind. It is also a challenge for HR departments to ensure good employment conditions for people of peri-retirement age - encouraging 60+ people to remain active in the labour market despite the possibility of retirement.

In a brief summary, we can say that despite the many challenges the industry faced in 2023 - in the form of inflation, ongoing wars around the world and our borders, the unstable political situation in Poland related to the elections - the FMCG industry remained stable in terms of volume, recording price-driven growth. Polish consumers tried to save - which translated into volume declines in some categories and growth in other areas - technology, private labels, promotional mechanisms. The next year will see further work on sustainability commitments, work on assortment optimisation, inclusivity of the offer - in the face of a polarising society economically and demographically. Hopefully, in all the challenges, we will be supported by artificial intelligence.

Konrad Wacławik

Head of Retailer Services, NielsenIQ

From a global perspective, the FMCG market in 2023 grew by nearly 9% in terms of sales value (analysing the 12 months to the end of September 2023). Market dynamics in Europe also achieved a similar result. In Poland, the FMCG market grew by 11.7% year-on-year in value terms in the last 52 weeks ending 10.12.2023. One can venture the opinion that in the face of all the challenges - this is a positive double-digit market value growth. Unfortunately, looking at the sales volume in the perspective of the Polish FMCG market in 2023, we are rather talking about stagnation or even a slight decline - especially in Q1 and Q2 (which, in the previous year, saw the outbreak of war in Ukraine and a large migration of citizens from Ukraine to Poland).

The year 2023 also saw the continuation of trends already known on the Polish retail market - the strengthening of the position of discount stores, which, taking into account the sum of food, chemical, cosmetic and tobacco products, reached a weight of 38% of the market, recording an increase of over 18% in the value of sales. Supermarkets, drugstore chains and online sales channels also recorded significant sales growth. Taking into account sales from the largest marketplaces - the importance of the online channel in Poland in selected cosmetic categories according to NielsenIQ - e.g. body care or facial care - is already close to 15% of the total market. This confirms that the trend, which has been with us for a long time and has been booming since the pandemic, of some sales categories moving to ecommerce, has already reached a significant level.

Despite a drop in inflation in the second half of the year (to 6.5% in November 2023 according to the Central Statistical Office) - Polish consumers have spent this past year perfecting their savings behaviour. Although grocery shopping decidedly did not appear as the first category on which we want to save - 56% of shoppers said in the September reading that they plan to save on FMCG products (source NIQ Shopper Trends Pulse 2023). This effect was visible in various dimensions - some categories such as alcohol - above all in the largest categories, i.e. beer and vodka, recorded declines in volume sales in 2023. Poles bought less alcohol than a year ago (an unprecedented situation in the last decade). Another area undoubtedly influenced by frugal attitudes is the chains’ private labels. The chains’ private brands-which still, in the opinion of shoppers, have the advantage of being cheaper products-recorded a 20% increase in the value of sales for food products (also supported by a slight increase in volume). The trend of increasingly choosing chain brands is also evident in other regions, globally private labels achieved a growth rate of 13% vs 9% of the entire basket including manufacturer products. Increasingly, we are also seeing dedicated advertising and marketing campaigns targeting specific brands of the chain’s own brands - showing that these brands are often already leaders in their categories. The third common behaviour of shoppers managing their budget was to actively seek out promotions. The share of promotions in the FMCG basket in Poland did not increase compared to the previous year - in the hypermarket and supermarket market, it remained at 33% of value sales made during promotions. However, consumer expectations of promotions are increasing - the importance of an attractive promotional offer is rising in the ranking of factors influencing shop choice. This forces chains and suppliers to pursue a very targeted and effective promotional and pricing policy, often tailored to the location, shopper or current market need.

We are entering 2024 with optimism, bidding a hopeful farewell to double-digit inflation, looking forward to a more stable and predictable political situation and hoping that consumers will slightly loosen the hitherto restrictive attempts to keep their money in their wallets and be able to shop more often on Sundays (if the promises of the current coalition are fulfilled). What can we expect from trends in the FMCG market?

Taking into account the lessons of the 2007-2010 economic crisis, we can expect learned savings mechanisms to remain with Polish consumers even if their economic situation improves in the coming years. This may give rise to several changes in the market - one of which will be a redefinition of price levels and assortment - adjusting the offer to a more polarised society, where an important group of consumers can afford premium products and an equally large group, will look for a more economical offer. The search for promotions and the development of technology has meant that already the vast majority of shoppers are also taking advantage of loyalty or points programmes offered by retail chains. Development in this area will also be an important trend in 2024, bearing in mind the need to control spending and buy products with tailored and attractive offers will also remain with us.

A significant challenge that the FMCG industry will have to deal with in 2024 is also, rightly, the pressure to move towards climate neutrality. The packaging deposit system introduced is just one element related to the industry’s commitments, which will affect a significant proportion of the FMCG sectors. Caring for the planet and being in line with the European Green Deal also ties in with the trend towards health and general wellbeing - which will also be an important market driver in the coming years. In the short term, we will observe the impact of regulations banning the sale of energy drinks to minors, while in the long term, products guaranteeing a proactive approach to health or responding to civilisation-related illnesses have growth potential (we can already see specialist Superharm medical centres appearing on the Polish market or promotional campaigns for health-oriented products undertaken by, for example, Amazon).

The development of the FMCG market in 2024 and beyond must also take into account the demographic changes in society. In 2030, 54% of FMCG spending will be carried out by the 50+ group, which will of course be an active and very aware social group. It will be worth using these remaining few years to develop offers aimed at the ‘silver generation’, and to create technologies and solutions with older consumers in mind. It is also a challenge for HR departments to ensure good employment conditions for people of peri-retirement age - encouraging 60+ people to remain active in the labour market despite the possibility of retirement.

In a brief summary, we can say that despite the many challenges the industry faced in 2023 - in the form of inflation, ongoing wars around the world and our borders, the unstable political situation in Poland related to the elections - the FMCG industry remained stable in terms of volume, recording price-driven growth. Polish consumers tried to save - which translated into volume declines in some categories and growth in other areas - technology, private labels, promotional mechanisms. The next year will see further work on sustainability commitments, work on assortment optimisation, inclusivity of the offer - in the face of a polarising society economically and demographically. Hopefully, in all the challenges, we will be supported by artificial intelligence.

Konrad Wacławik

Head of Retailer Services, NielsenIQ