Nestlé continues to invest in future growth and operating efficiency, targeting mid-single digit organic growth and significant structural cost savings by 2020.”

Group results

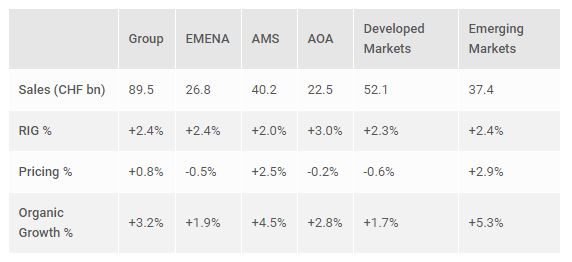

Sales

- Total sales increased by 0.8% to CHF 89.5 billion, with a foreign exchange impact of -1.6%. Acquisitions net of divestitures reduced sales by 0.8%.

- Organic growth was 3.2%, with real internal growth reaching a three-year high of 2.4%.

- Pricing was limited at 0.8%, with some improvement in the second half of the year. Pricing is expected to improve further for the full year 2017.

- Organic and real internal growth were broad-based, highlighting the strength and resilience of our diversified portfolio.

- Innovation supported volume growth, with 30% of sales coming from products introduced or renovated in the last 3 years.

- E-commerce accounted for 5% of sales, up 18% year-on-year.

Trading operating profit

- Trading operating profit was CHF 13.7 billion with a margin of 15.3%, up 20 basis points on a reported basis and up 30 basis points in constant currency.

- We achieved this margin improvement while:

- Investment increased in brand support, digital marketing, research and development, and in the new nutrition and health platforms. Consumer-facing marketing spend increased by 6.3% in constant currency.

- Restructuring costs doubled to CHF 300 million in 2016 to support structural cost-saving initiatives.

Net profit

- Net profit of CHF 8.5 billion was impacted by several items, the largest one being a one-off non-cash adjustment to deferred taxes.

- Reported earnings per share decreased by 4.8% to CHF 2.76, for the same reasons.

- Underlying earnings per share in constant currency increased by 3.4%.

Cash flow and working capital

- Operating cash flow improved by CHF 1.3 billion to CHF 15.6 billion (17.4% of sales) due in part to the reduction of working capital. Free cash flow improved by CHF 200 million to CHF 10.1 billion (11.3% of sales). This demonstrates our ability to generate strong cash flow consistently even in a challenging foreign exchange environment.

- Average working capital decreased by 190 basis points from 4.7% to 2.8% of sales (average of last five quarters).

- ROIC including goodwill and intangible assets improved by 30 basis points to 11.2%. ROIC before goodwill and intangible assets improved by 180 basis points to 31.7%.

Zone AMS

Sales of CHF 26.4 billion, 4.2% organic growth, 1.3% real internal growth; 19.3% trading operating profit margin, -10 basis points

- The Zone reported good and consistent organic growth.

- In North America growth accelerated year-on-year:

- In petcare, innovation supported good growth across the cat food range. In dog food, the premium portfolio performed well as Merrick, Purina ONE and Pro Plan all delivered double-digit growth. Beneful stabilised as there was progress in restaging the brand.

- Coffee Mate sustained good momentum through innovations such as 64 oz. and new flavours in natural bliss.

- Lean Cuisine and Stouffer’s Fit Kitchen delivered strong organic growth supported by new line extensions.

- The performance of confectionery in the US was disappointing, impacted by the competitive environment and low growth in the mainstream chocolate market.

- In Latin America strong organic growth was led by price increases following currency depreciation, as real internal growth slowed:

- In Brazil we had high single-digit organic growth. Significant price increases at the end of the first half of the year impacted volumes in the short term. Nescafé Dolce Gusto and KitKat continued to grow in double digits.

- In Mexico there was another year of good growth, which was broad-based across dairy, coffee creamers, soluble coffee, Nescafé Dolce Gusto and chocolate.

- Petcare continued to deliver strong growth across the region.

- The trading operating profit margin decreased by 10 basis points, due to an increase in restructuring costs. The profitability margin improved in North America, but Latin America was largely affected by high cost inflation caused by currency depreciation and commodity prices.

Zone EMENA

Sales of CHF 16.2 billion, 2.0% organic growth, 2.7% real internal growth; 16.7% trading operating profit margin, +100 basis points

- The Zone delivered strong real internal growth, accelerating for a fourth consecutive year and gaining market share, showing the ability to innovate.

- In Western Europe positive organic growth was due to solid real internal growth. Pricing was negative, affected by sustained low commodity prices, trade pressure and intense competition:

- Petcare, Nescafé and pizza continued to be the key sources of growth across most markets.

- In Germany and France we had solid real internal growth, while there was good organic and real internal growth in Southern Europe. In the UK, on the other hand, it was a particularly challenging year with both volume and pricing declining slightly.

- Central and Eastern Europe continued to deliver strong organic growth on the basis of good real internal growth and positive pricing:

- In Russia we achieved double-digit organic growth with positive real internal growth. This included strong growth in Nescafé soluble coffee, especially Barista. Russia was Nestlé’s strongest performing market in petcare globally, led by Felix cat food.

- Inflation in Russia and Ukraine drove positive pricing in the region, whilst all other markets experienced deflationary pricing.

- Business remained resilient in the Middle East and North Africa with positive organic growth, but the unstable environment and deflationary pressure slowed momentum:

- Events in Iraq, Yemen, Libya and Syria continued to have an effect. There was also deflationary pressure on dairy in the region.

- In Turkey Nescafé and confectionery drove double-digit growth. The North Africa market also did well.

- The trading operating profit margin improved by 100 basis points even as restructuring costs and marketing investment increased. Profitability improved across most categories as a result of premiumisation, volume leverage, efficiency savings and favourable input costs. Portfolio management also contributed positively with the creation of the Froneri joint venture in ice cream.

Zone AOA

Sales of CHF 14.5 billion, 3.2% organic growth, 2.9% real internal growth; 19.0% trading operating profit margin, +60 basis points

- The Zone saw real internal growth and organic growth gain increasing momentum throughout the year, with market shares recovering and almost all markets contributing.

- The Zone’s emerging markets had a good year overall with growth accelerating in most businesses. Yinlu was the main exception, decreasing the Zone’s organic growth by 260 basis points:

- In China the double-digit decline of Yinlu affected overall growth. Several initiatives to turn around the business are in place and stabilisation is expected in 2017. Dairy (excluding Yinlu) and confectionery grew positively and Nescafé performed well.

- South East Asia was strong with double-digit growth in Vietnam and Indonesia, especially from dairy and Milo. The Philippines also performed well with high single-digit growth, particularly due to Bear Brand in dairy.

- There was good growth in sub-Saharan Africa. Real internal growth remained positive despite price increases to offset currency depreciation. There was double-digit growth in Central and West Africa (including Ghana, Côte d’Ivoire and Nigeria) and in Equatorial Africa (including Angola), with Maggi and Nido doing well.

- Our business in India grew strongly despite some disruptive impact from demonetisation at the end of the year. Maggi noodles continued to regain market share. Confectionery also did well with KitKat. There was also strong growth in Pakistan from dairy, ready-to-drink and other categories.

- In the developed markets there was good growth in Japan and solid real internal growth in Oceania:

- Japan’s organic growth was above the Zone and Group averages, balanced evenly between real internal growth and pricing. This was based on innovation and premiumisation across Nescafé and KitKat.

- In Oceania there was solid real internal growth in line with the Group, which was largely offset by continuing deflationary pressure.

- The Zone improved its trading operating profit margin by 60 basis points while also increasing marketing investment. Positive gross margin development was helped by favourable input costs, particularly in dairy, as well as cost efficiencies and improved volumes and product mix. The effect of an increase in restructuring spend was more than offset by lower one-off costs related to Maggi in India.

Nestlé Waters

Sales of CHF 7.9 billion, 4.5% organic growth, 4.5% real internal growth; 11.9% trading operating profit margin, +110 basis points

- Nestlé Waters maintained its good organic growth momentum based on real internal growth. Pricing remained flat:

- In the US, international premium brands saw another year of dynamic growth and there were contributions above the Group and Nestlé Waters averages from regional brands Poland Spring, Ice Mountain and Deer Park. The shutdown of a factory in Texas following a tornado in April had a negative impact.

- In Europe, the majority of markets maintained growth after 2015 had been a strong year due to the heatwave. There were good contributions from the UK, Spain and Germany.

- Of the other markets, South East Asia, Mexico and North Africa did well.

- Further strong growth came from the international premium sparkling brands Perrier and S.Pellegrino, which grew twice as fast as the mainstream portfolio.

- The flagship international brand Nestlé Pure Life made a good contribution, with organic growth above the Nestlé Waters average.

- There was a strong trading operating profit margin improvement of 110 basis points while marketing investment also increased. This was possible due to a combination of volume growth, positive product mix through premiumisation, operational cost efficiencies and favourable input costs.

Nestlé Nutrition

Sales of CHF 10.3 billion, 1.5% organic growth, 0.9% real internal growth; 22.7% trading operating profit margin, +10 basis points

- Nestlé Nutrition grew in the context of changed category dynamics, particularly in China, and deflationary pressure owing to sustained low milk prices:

- Market dynamics in China were weak ahead of the implementation of new regulation, resulting in adjustments of trade inventory levels in both mainland China and Hong Kong. Low dairy prices and intense competition had an impact on pricing, particularly in the premium segment. At the same time, illuma had another strong year of growth, gaining share to become the leading brand in its category in China. We also strengthened our capabilities in e-commerce, winning market share in this important channel.

- Growth in the US was slow during the year. We started to renovate the Gerber brand and made improvements to product packaging and recipes, including many organic offerings.

- Latin America saw strong momentum led by innovations such as Mucilon Iron Plus cereals in Brazil and NAN Optipro in Mexico.

- Growth in South East Asia was also solid with the Philippines doing well.

- The improvement in trading operating profit margin was broad-based across infant formula as well as baby food, due to sustained low dairy prices. At the same time, marketing investment behind brands increased.

Other businesses

Sales of CHF 14.1 billion, 3.7% organic growth, 3.4% real internal growth; 15.2% trading operating profit margin, -50 basis points

- Nestlé Professional continued to grow, led by mid-single-digit growth in emerging markets with strong growth in Russia and Mexico and solid growth in China. The US also had good organic growth while business in Canada and Western Europe declined. As from 2017, Nestlé Professional is integrated into the Zones due to increasing demand for more customised products and services on a local and regional basis.

- Nespresso continued to grow in its 30th year. The US and Canada saw strong momentum from the continued success of the VertuoLine system. Sales in France also benefitted from the launch of VertuoLine at the end of the year. The UK saw strong acceleration following brand investment and the launch of a subscription model. In Asia, both China and Korea performed well.

- Nestlé Health Science maintained a good pace of growth. Consumer care was once again the key source of growth including the Boost range of products, Carnation Breakfast Essentials and, in Europe, Meritene. Medical nutrition benefitted from strong contributions from the allergy portfolio (especially in China), Vitaflo and oral nutritional supplements in key markets.

- Nestlé Skin Health performed well in consumer care. However, we adjusted inventory levels in the trade at the end of the year. Increased competition and pressure from generics affected the US prescription business.

- The trading operating profit margin of this segment was impacted by Nestlé Skin Health. Adjustment of trade inventories and higher restructuring and litigation costs affected profitability. Nestlé Health Science also absorbed higher restructuring costs. Nestlé Professional and Nespresso both improved their profitability, helped by favourable input costs.

Board proposals to the Annual General Meeting

At the Annual General Meeting on 6 April 2017, the Board of Directors will propose a dividend of CHF 2.30 per share. The last trading day with entitlement to receive the dividend will be 7 April 2017. The net dividend will be payable as from 12 April 2017. Shareholders who are on record in the share register with voting rights on 30 March 2017 at 12:00 noon (CEST) will be entitled to exercise their voting rights.

On 27 June 2016, the Board announced its succession plans for the Chairman and the CEO. After serving the company for almost 50 years, including 11 years as CEO and 12 years as Chairman, Peter Brabeck-Letmathe will not stand for re-election as he has reached the mandatory retirement age. The Board proposed Paul Bulcke, who served as CEO from 2008 to end of 2016, for election as Chairman. On 27 June 2016, the Board also appointed Mark Schneider as Nestlé CEO starting on 1 January 2017. In line with the Company’s proven governance model, he has been proposed for election to the Board at the Annual General Meeting.

The Board is proposing the individual re-election of the other current members of the Board of Directors for a term of office until the end of the next Annual General Meeting. In addition, the Board is proposing the election of Ursula M. Burns (pdf, 14 Kb), Chairman of the Board of Xerox Corporation since 2010 and its CEO from 2009 to 2016.

Finally, the Board is proposing the individual election of the members of the Compensation Committee and the election of KPMG as statutory auditors until the end of the next Annual General Meeting. The Board is also submitting the compensation of the Board of Directors and the Executive Board for approval by shareholders.

Outlook

In 2017, we expect organic growth between 2% and 4%. In order to drive future profitability, we plan to increase restructuring costs considerably in 2017. As a result, the trading operating profit margin in constant currency is expected to be stable. Underlying earnings per share in constant currency and capital efficiency are expected to increase.

Annex

Full-year 2016 sales and trading operating profit margins overview

surce: nestle.com