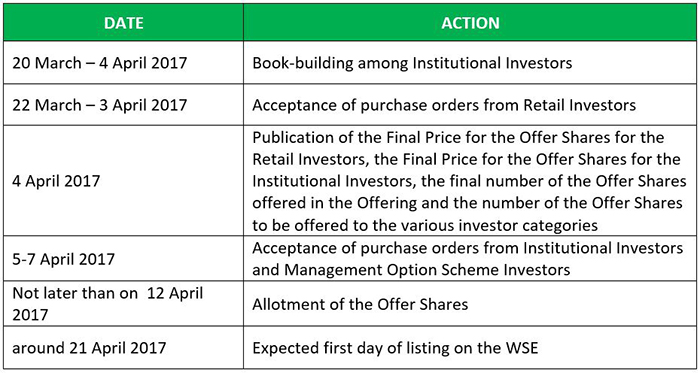

The book-building process among Institutional Investors will be conducted between 20 March and 4 April 2017. PKO BP Securities, UBS Investment Bank, and Wood & Company Financial Services, a.s. Spółka Akcyjna (Oddział w Polsce) will act as Joint Global Coordinators and Joint Bookrunners. Erste Group Bank AG will be acting as a Joint Bookrunner. The Offering Agent and the Stabilizing Manager will be PKO BP Securities.

Retail investors can place purchase orders between 22 March and 3 April 2017 at selected Customer Service Locations of PKO BP Securities and other investment firms joining the Retail Consortium in Poland and accepting purchase orders for Offer Shares from Retail Investors. The Retail Consortium includes: PKO BP Securities, Biuro Maklerskie Alior Banku, Dom Maklerski Banku Ochrony Środowiska, Centralny Dom Maklerski Pekao, Dom Maklerski Pekao, Dom Maklerski BZ WBK and Dom Maklerski mBanku.

INDICATIVE SUMMARY TIMETABLE OF OFFERING

DETAILS OF THE PUBLIC OFFERING

DINO’S STRATEGY

Dino’s strategy assumes further growth through focusing on three key areas:

COMPETITIVE STRENGTHS

The Company plans to pursue its growth strategy through further exploitation of the chain’s strengths and competitive advantages, which include:

NUMBER OF STORES EVOLUTION

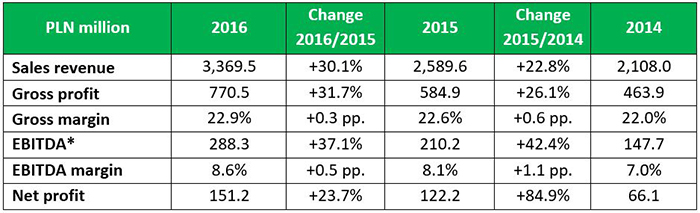

FINANCIAL RESULTS

*EBITDA defined as operating profit plus depreciation and amortization adjusted for one-off items, including reserves in relation to the new management incentive plan and other Offering-related one-off expenses in the total amount of PLN 7.5m in 2016.

*EBITDA defined as operating profit plus depreciation and amortization adjusted for one-off items, including reserves in relation to the new management incentive plan and other Offering-related one-off expenses in the total amount of PLN 7.5m in 2016.

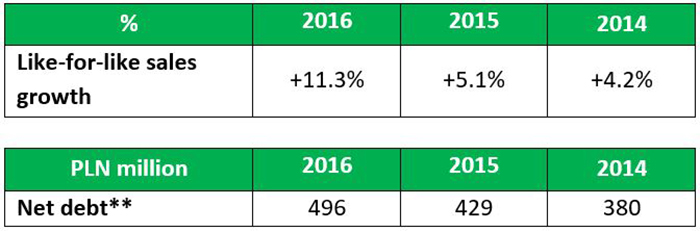

** The Dino Group defines net debt as interest-bearing loans, borrowings and finance lease liabilities + current portion of interest-bearing loans and finance lease liabilities less any cash and cash equivalents. The net debt ratio is the measure of the indebtedness of the Dino Group less cash and cash equivalents.

** The Dino Group defines net debt as interest-bearing loans, borrowings and finance lease liabilities + current portion of interest-bearing loans and finance lease liabilities less any cash and cash equivalents. The net debt ratio is the measure of the indebtedness of the Dino Group less cash and cash equivalents.

MARKET ENVIRONMENT

Retail food market

In 2010-2015 the market for retail trade in grocery items in Poland grew at an average annual rate of 3.4%. The traditional grocery segment fell on average by 7.7% per year, while the modern segment increased its market share by 15 pp. Overall grocery retail sales in Poland are expected to grow at an average annual rate of 3.7% through 2020.

The observed growth in the Polish grocery market is an effect of the encouraging macroeconomic situation, growing disposable income, and related growth in consumer spending. The government’s Family 500+ program, declining unemployment, and regular increase in the minimum wage support individual consumption in Poland. This is particularly observed in the smaller towns where Dino stores are located.

Proximity segment

The segment of proximity supermarkets, in which the Dino Group operates, is the fastest-growing segment of the retail grocery market in Poland in terms of the number of stores. In 2010-2015 this segment generated CAGR (annual growth) of 13.2%. It is expected that this segment will be the fastest-growing segment in 2015-2020 in terms of CAGR in the number of stores, at about 10.7%.

Proximity supermarkets in Poland are operated mainly as general grocery stores with an area of 200 to 500 m2, in the form of a hard franchise or owned stores, offering 4,000-8,000 stock-keeping units, about 90% of which are food items. They are typically located near residential zones in large, medium-sized and small towns.

Proximity supermarkets are successfully growing in Poland for the following reasons:

- they have an advantage over larger-format stores, particularly hypermarkets and large supermarkets, resulting from a more convenient location for customers and the ability to complete their shopping in a much shorter time;

- they offer a broader assortment than discount chains or convenience stores;

- they have an advantage over independent grocery stores resulting from centralized logistics and the scale of purchasing.

All of these advantages led to doubling of the share of proximity supermarkets in the Polish grocery market in 2010-2015 in terms of the number of stores (source: Roland Berger report).

Szymon Piduch, CEO of Dino Polska S.A., commented: “We are one of the fastest-growing supermarket chains in Poland, operating in the promising proximity segment. We are growing dynamically, and increased the number of stores from 111 at the end of 2010 to 628 at the end of 2016, while maintaining very good LFL sales figures. I believe that Dino has very good prospects for further growth. We estimate that the Polish market has the capacity for at least 2,700 Dino stores, and we plan to exceed 1,200 stores by the end of 2020. We plan additional investments supporting the opening of new stores, including construction of new distribution centre, modernization and expansion of the existing meat-processing plant operated by Agro-Rydzyna, and construction of another meat plant at a new location. It is also our goal to maintain continued growth in like-for-like sales and consistent improvement in profitability. I believe that the Company can be attractive for investors. The steady increase in the scale of operations since the beginning of Dino’s existence has shown that we are effectively realizing our strategic goals.”

Retail investors can place purchase orders between 22 March and 3 April 2017 at selected Customer Service Locations of PKO BP Securities and other investment firms joining the Retail Consortium in Poland and accepting purchase orders for Offer Shares from Retail Investors. The Retail Consortium includes: PKO BP Securities, Biuro Maklerskie Alior Banku, Dom Maklerski Banku Ochrony Środowiska, Centralny Dom Maklerski Pekao, Dom Maklerski Pekao, Dom Maklerski BZ WBK and Dom Maklerski mBanku.

INDICATIVE SUMMARY TIMETABLE OF OFFERING

DETAILS OF THE PUBLIC OFFERING

- The Offering will consist of no more than 48,040,000 existing series A ordinary shares (the “Offer Shares”), representing 49% of the Company’s share capital, owned by the Selling Shareholder, Polish Sigma Group S.à r.l. with its registered office in Luxembourg (belonging to Polish Enterprise Fund VI, managed by Enterprise Investors) (the “Selling Shareholder”). The Offering does not involve a capital increase or raising of additional capital by Dino.

- It is anticipated that after completion of the Offering, Tomasz Biernacki (Dino’s founder), holding 50,000,000 ordinary shares representing 51% of the Company’s share capital, will remain the Company’s majority shareholder.

- The Offering will be addressed to Retail Investors and Institutional Investors in Poland, and to selected foreign Institutional Investors outside of the United States in reliance on Regulation S under the U.S. Securities Act of 1933 (the “Securities Act”) and to qualified institutional buyers in the United States pursuant to and subject to the requirements of Rule 144A of the Securities Act.

- It is anticipated that Retail Investors will be able to acquire a total of about 5% of the total number of Offer Shares finally allotted in the Offering.

- The Offering will also be addressed to Management Option Scheme Investors, being Management of Dino Polska S.A. covered by the Management Option Schemes who will be able to file purchase orders under the same conditions as for Institutional Investors.

- The shares belonging to Tomasz Biernacki will be subject to a lock-up agreement for a period of 720 days from the date of the first listing of the Company’s shares on the WSE. Any shares purchased by members of the Management Board of the Company and other senior managers of the Company being participants of the incentive schemes (as Management Option Scheme Investors) in the IPO will be subject to a two-year lock-up agreement from the date of the first listing of the Company’s shares on the WSE. In case the Selling Shareholder holds any shares in the Company following the Offering, it will be subject to a lock-up period of 180 days from the date of the first listing of the Company’s shares on the WSE. The Company will be subject to a 360-day lock-up period from the date of the first listing of the Company’s shares on the WSE in respect of any new issuance of shares.

- The Company’s shares will be listed on the regulated (main) market of the WSE.

DINO’S STRATEGY

Dino’s strategy assumes further growth through focusing on three key areas:

- Continued fast organic growth in the number of stores. The Company believes there is a market capacity for at least 2,700 Dino stores in Poland and plans to exceed the number of 1,200 stores by the end of 2020.

Dino plans to continue its strategy of ownership of the majority of store premises and leveraging its organic roll-out capabilities in the current format by increasing the density of store coverage in the current areas of operation and gradual expansion towards new regions in Poland.

The Company intends to make additional investments supporting the roll-out of new stores, including construction of a fourth distribution centre by the end of 2018 and modernization and expansion of the existing meat processing plant of Agro-Rydzyna and construction of another meat processing plant in a new location (by the end of 2020). - Continued delivery of LFL sales growth. Dino expects to be able to continue to deliver LFL sales growth. To achieve this objective, the Company will take actions aimed at increasing the number of shoppers in Dino stores and the value of sales per shopper.

Key trends affecting changes in consumers’ lifestyles and grocery shopping habits supporting the foregoing plans, according to industry reports, include:

- seeking shops near where they live and shopping convenience;

- demand for higher-quality and branded products;

- increasing health consciousness and focus on fresh and healthy food, including local Polish products.

The proximity format adopted by the Dino Group and the Company's strategy address these consumer trends. - Continued improvement in profitability. In 2014-2016 Dino generated a consistent increase in its gross and EBITDA margins, and expects to be able to continue to improve profitability through increasing the scale of the business, favourable characteristics of its business model, and a number of strategic initiatives. These include:

- economies of scale leading to further gross margin growth due to fast roll-out of the Company’s stores network and increased LFL sales and, consequently, rapidly increasing purchasing volumes helping to improve purchasing terms;

- increased cost efficiency at the single-store level achieved through taking regular actions aimed at cutting the costs of store operation;

- significant operational leverage leading to further growth in the EBITDA margin due to a number of relatively fixed cost items growing at a lower rate than sales;

- planned investment in optimization of the logistics network shortening delivery routes and leading to a further decrease in transport costs relative to sales.

COMPETITIVE STRENGTHS

The Company plans to pursue its growth strategy through further exploitation of the chain’s strengths and competitive advantages, which include:

- Leading position in the fast-growing proximity supermarket segment in Poland

- Proven rapid network roll-out capabilities based on own real estate

- Outstanding offer of fresh and branded products and competitive pricing

- Cost-effective and scalable business model

- Proven track record of strong financial performance

- Experienced management team

NUMBER OF STORES EVOLUTION

FINANCIAL RESULTS

MARKET ENVIRONMENT

Retail food market

In 2010-2015 the market for retail trade in grocery items in Poland grew at an average annual rate of 3.4%. The traditional grocery segment fell on average by 7.7% per year, while the modern segment increased its market share by 15 pp. Overall grocery retail sales in Poland are expected to grow at an average annual rate of 3.7% through 2020.

The observed growth in the Polish grocery market is an effect of the encouraging macroeconomic situation, growing disposable income, and related growth in consumer spending. The government’s Family 500+ program, declining unemployment, and regular increase in the minimum wage support individual consumption in Poland. This is particularly observed in the smaller towns where Dino stores are located.

Proximity segment

The segment of proximity supermarkets, in which the Dino Group operates, is the fastest-growing segment of the retail grocery market in Poland in terms of the number of stores. In 2010-2015 this segment generated CAGR (annual growth) of 13.2%. It is expected that this segment will be the fastest-growing segment in 2015-2020 in terms of CAGR in the number of stores, at about 10.7%.

Proximity supermarkets in Poland are operated mainly as general grocery stores with an area of 200 to 500 m2, in the form of a hard franchise or owned stores, offering 4,000-8,000 stock-keeping units, about 90% of which are food items. They are typically located near residential zones in large, medium-sized and small towns.

Proximity supermarkets are successfully growing in Poland for the following reasons:

- they have an advantage over larger-format stores, particularly hypermarkets and large supermarkets, resulting from a more convenient location for customers and the ability to complete their shopping in a much shorter time;

- they offer a broader assortment than discount chains or convenience stores;

- they have an advantage over independent grocery stores resulting from centralized logistics and the scale of purchasing.

All of these advantages led to doubling of the share of proximity supermarkets in the Polish grocery market in 2010-2015 in terms of the number of stores (source: Roland Berger report).

Szymon Piduch, CEO of Dino Polska S.A., commented: “We are one of the fastest-growing supermarket chains in Poland, operating in the promising proximity segment. We are growing dynamically, and increased the number of stores from 111 at the end of 2010 to 628 at the end of 2016, while maintaining very good LFL sales figures. I believe that Dino has very good prospects for further growth. We estimate that the Polish market has the capacity for at least 2,700 Dino stores, and we plan to exceed 1,200 stores by the end of 2020. We plan additional investments supporting the opening of new stores, including construction of new distribution centre, modernization and expansion of the existing meat-processing plant operated by Agro-Rydzyna, and construction of another meat plant at a new location. It is also our goal to maintain continued growth in like-for-like sales and consistent improvement in profitability. I believe that the Company can be attractive for investors. The steady increase in the scale of operations since the beginning of Dino’s existence has shown that we are effectively realizing our strategic goals.”