In the reporting year, like-for-like Group sales rose by 1.5% and EBIT before special items totalled €1,511 million, while negative exchange rate effects amounted to €117 million altogether. METRO GROUP therefore significantly exceeded the comparable previous year’s figure of €1,414 million adjusted for currency effects. As a result, the company met its sales and earnings targets for the financial year. “The successes of our transformation have become clearly evident in terms of operations,” says Olaf Koch, Chairman of the Management Board of METRO AG. “We have managed to achieve sustainable positive sales development for METRO Cash & Carry as well as for Media-Saturn, which is reflected accordingly in the earnings position as measured in local currency. Last but not least, we have switched our course back to growth again with the acquisitions of Classic Fine Foods and RTS. We will continue to pursue this strategy in 2015/16 and place even greater focus on our customers’ needs. In addition, we will further remodel and modernise many of the stores of our sales lines, take advantage of promising acquisitions and also look at new expansion targets again,” Koch said.

By significantly reducing its net debt by €2.2 billion, METRO GROUP has further strengthened its balance sheet and thereby opened up room for making future investments. Plans call for raising the dividend of €0.90 per ordinary share in the previous financial year to €1.00 to include shareholders in METRO GROUP’s improved economic situation.

Thanks to the systematic implementation of their strategies, in addition to a number of measures and initiatives, the sales lines contributed to the successful development of METRO GROUP in financial year 2014/15.

METRO Cash & Carry focused even more towards the needs of its professional customers in financial year 2014/15 and succeeded in further expanding its delivery business, among other things. Sales from the delivery business rose by 13.7% to €3.1 billion (2013/14: €2.8 billion). Delivery sales accounted for 10.6% of METRO Cash & Carry’s total sales. Another milestone was the acquisition of Classic Fine Foods (CFF), one of the leading Asian providers in the high-growth food delivery business. Headquartered in Singapore, Classic Fine Foods directly supplies food to companies from the hotel, restaurant and catering (Horeca) segment.

METRO Cash & Carry also made important progress in terms of digitalsation. In order to be able to offer commercial customers of METRO Cash & Carry new services and technologies in future, METRO GROUP started the Techstars METRO Accelerator in financial year 2014/15. The support programme is being jointly implemented with US company Techstars, one of the most internationally renowned start-up networks, as well as the digital agency R/GA. The Techstars METRO Accelerator is geared towards founders with innovative technological applications for the Horeca segment. As part of the programme, experienced mentors and experts support selected start-up companies in successfully developing their own business within three months.

Since April 2015 METRO GROUP has also a stake in the US online job network Culinary Agents, a networking and job matching site for food, beverage and hospitality professionals. Due to the cooperation with METRO Cash & Carry this service is now offered in Italy and France since October for the first time.

In financial year 2014/15, Media-Saturn further accelerated its transformation from a primarily stationary provider of consumer electronics into a successful multi-channel retailer. The share of Media-Saturn sales generated online rose to more than 8%. The sales line is now represented by more than 1,000 stationary Media Markt and Saturn locations. With new formats such as Saturn Connect, which is a more compact city centre format focused on mobile communications, laptops, computers and other digital devices, Media-Saturn is also responding successfully to trends in traditional retailing. To further expand services for its customers, Media-Saturn acquired the majority stake in customer and repair service provider RTS in August 2015. RTS provides services for electronic products across Germany as well as through partners across Europe. The service range includes planning, installation, inspection, maintenance and repair for a wide variety of such products.

Real celebrated its 50th anniversary in financial year 2014/15. After hosting kick-off events at stores and central locations, the hypermarkets held discount campaigns and special promotional weeks dedicated to freshness, variety and innovation for their customers all year long. At the same time, the hypermarket operator continued to concentrate on enhancing the competitiveness of its locations and making them fit for the future. The locations that have been remodelled in keeping with the design of the Essen store are a key driver in these efforts. In financial year 2014/15, the successful concept was introduced at 57 additional Real stores. Real now operates 107 of these modern locations. Plans are being made to remodel more stores. Real also made progress with regard to a more competitive cost structure. A significant portion of product invoicing is now handled by Switzerland-based company Markant, which makes it possible to take advantage of standardisation and efficiency benefits.

Progress with portfolio optimisation successfully continued

METRO GROUP successfully continued to optimise its portfolio in financial year 2014/15. The most important transaction in this regard was the sale of Galeria Kaufhof¹, concluded on 30 September 2015. The purchase price was €2.825 billion, including various liabilities. The net cash inflow of €1.75 billion and the book profit of €0.8 billion exceeded the original forecast.

Additional measures aimed at focusing the portfolio in financial year 2014/15 were the sale of the wholesale business in Denmark as well as the disposal of the wholesale business in Greece. All of the documents necessary for the approval of the sale of the wholesale business in Vietnam have been submitted.

Business development 2014/15

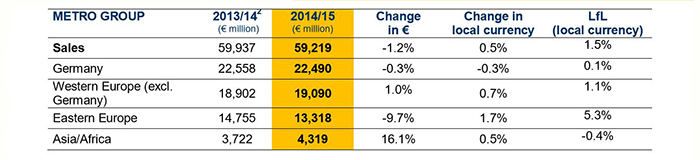

METRO GROUP sales rose by 1.5% on a like-for-like basis in financial year 2014/15. Sales in local currency grew by 0.5%. However, the reported sales of €59.2 billion were down on the previous year’s figure by 1.2% due to negative exchange rate and portfolio effects. In Germany, like-for-like sales were on par with the previous year. At €22.5 billion, sales were down slightly overall on the previous year by 0.3%. This development was the result of a decline in sales at METRO Cash & Carry and Real. In the case of Real, store closings had a negative impact on sales. In contrast, Media-Saturn sales increased.

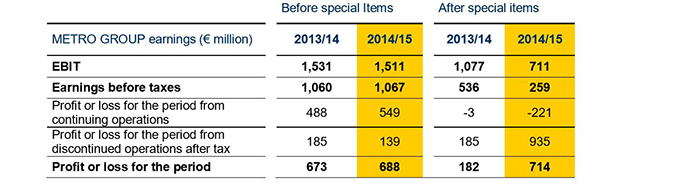

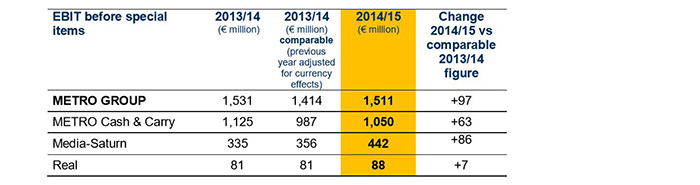

At €711 million, METRO GROUP’s EBIT fell short of the previous year’s level by €366 million in financial year 2014/15 (2013/14: €1,077 million). However, this figure included special items of €800 million (2013/14: €454 million). These special items can be divided into goodwill impairment losses (especially with respect to Real Germany at €446 million), restructuring and efficiency enhancement measures totalling €285 million (primarily planned closings) and other special items of €66 million. In addition, there was a positive special item from portfolio measures that totalled €23 million. Discontinued operations also contributed a positive special item of €841 million, which resulted from the proceeds of selling Galeria Kaufhof. METRO GROUP’s EBIT before special items decreased from €1,531 million to €1,511 million in financial year 2014/15. It should be noted, however, that negative exchange rate effects amounting to €117 million strained earnings. EBIT before special items thus rose considerably when measured in local currency.

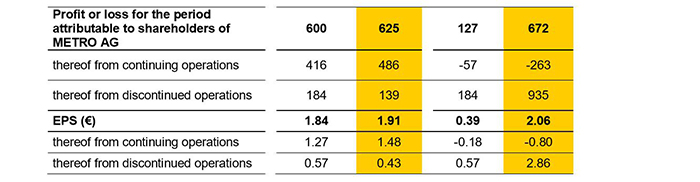

METRO GROUP’s profit or loss for the period amounted to €714 million in financial year 2014/15, which is €532 million higher than the previous year’s level (2013/14: €182 million). Net of non-controlling interests, profit or loss for the period attributable to the shareholders of METRO AG amounted to €672 million (2013/14: €127 million). This corresponds to a significant improvement of €545 million. Profit or loss for the period included special items of €í26 million (2013/14: €491 million). Adjusted for these special items, profit or loss for the period amounted to €688 million (2013/14: €673 million).

In financial year 2014/2015, METRO GROUP generated improved earnings per share of €2.06 (2013/14: €0.39). EPS before special items amounted to €1.91 (2013/14: €1.84). This result provides the basis of the dividend proposal. On 25 November 2015, METRO AG already announced a change to its dividend policy. Due to METRO GROUP’s improved economic situation, plans call for raising the distribution ratio from the current range of around 40 to 50% to around 45 to 55%. The Management Board therefore intends to propose at the Annual General Meeting distributing a dividend of €1.00 per METRO ordinary share and €1.06 per METRO preference share for financial year 2014/15. This would correspond to a ratio of 52.4%.

METRO GROUP succeeded in considerably reducing its net debt year on year by €2.2 billion. Net debt totalled €2.5 billion as at 30 September 2015 (30 September 2014: €4.7 billion).

Outlook

The METRO GROUP forecast is based on the current group structure and refers to currency-adjusted figures. In addition, it is based on the assumption of a persistently complex geopolitical environment.

For financial year 2015/16, METRO GROUP expects to see a slight rise in overall sales, despite the continuously challenging economic environment. In like-for-like sales, METRO GROUP foresees another slight increase that will follow the reporting year’s rise of 1.5%. The sales lines METRO Cash & Carry and Media-Saturn in particular are expected to contribute to both total sales and like-for-like sales growth; we expect the Real sales line to improve its performance compared with the past financial year.

In financial year 2015/16, earnings development will also be shaped by the persistently challenging economic environment. Nevertheless, METRO GROUP is confident that it can again achieve an earnings increase as a result of the progress it has made and will continue to make in transforming its business models. Aside from operational improvements, METRO GROUP will again closely focus on efficient structures and strict cost management in this context in financial year 2015/16. For these reasons, we expect EBIT before special items to rise slightly above the €1,511 million achieved in financial year 2014/15, including income from real estate sales. METRO Cash & Carry and Media-Saturn in particular are expected to contribute to this development, while the development of the Real sales line will depend on the successful implementation of the measures that have been initiated.

METRO Cash & Carry

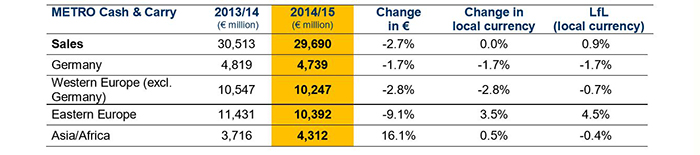

METRO Cash & Carry’s sales rose on a like-for-like basis by 0.9% in financial year 2014/15. In the process, it was possible to increase sales in every quarter. The previous year’s figure was matched in terms of sales in local currencies. Reported sales fell by 2.7% to €29.7 billion due to the development of exchange rates í primarily that of the Russian rouble í and portfolio effects.

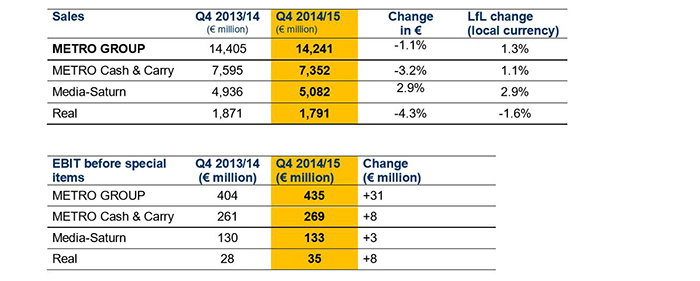

METRO Cash & Carry’s like-for-like sales continued to see very positive development in the fourth quarter of 2014/15, growing by 1.1%. This marks the ninth consecutive quarter of such growth. Negative exchange rate effects and store disposals caused reported sales to decrease by 3.2% to €7.4 billion. However, sales in local currency were on par with the same quarter in the previous year.

METRO Cash & Carry’s EBIT totalled €975 million in financial year 2014/15 (2013/14: €904 million) and included special items of €75 million (2013/14: €221 million) In particular, these items consisted of restructuring and efficiency enhancement measures, among others, at METRO Cash & Carry Germany. EBIT before special items amounted to €1,050 million (2013/14: €1,125 million). This decrease is due especially to negative exchange rate effects in Russia. Adjusted for these effects, earnings before special items improved.

Media-Saturn

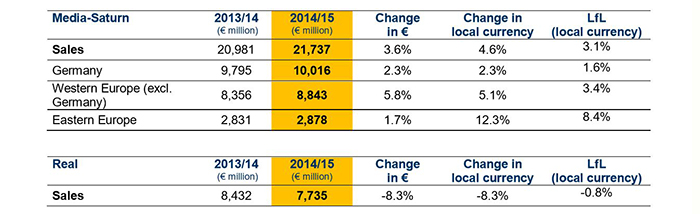

Media-Saturn’s sales rose on a like-for-like basis by 3.1% in financial year 2014/15. In the process, it was possible to increase sales on a like-for-like basis in every quarter of the financial year. Sales in local currency rose by 4.6%, and reported sales grew by 3.6% to €21.7 billion. Like-for-like sales at Media-Saturn improved by 2.9% in the fourth quarter of 2014/15, making it the fifth consecutive quarter of such growth. Reported sales increased by 2.9% to €5.1 billion (in local currency: +4.5%).

Online retail continued to see very dynamic development. Sales generated online rose by more than 20% and amounted to €1.8 billion. Online sales now account for more than 8% of Media-Saturn’s overall sales.

In Germany, like-for-like sales rose by 1.6%. Reported sales grew by 2.3% to €10.0 billion. The trend over the course of the year was extremely positive and was only dampend in summer due to a high level the previous year as a result of the FIFA World Cup. The further integration of the sales channels went over very well with customers. The pickup rate of goods purchased online was around 40%. The product range online was further expanded and at the end of September 2015 comprised more than 150,000 products at mediamarkt.de and some 130,000 products at saturn.de. As a result, the selection online now considerably exceeds the range offered at most Media-Saturn locations.

EBIT at Media-Saturn improved considerably to €336 million (2013/14: €244 million), which included special items of €107 million. These items consisted of numerous restructuring and efficiency enhancement measures. EBIT before special items rose appreciably from €335 million to €442 million. A better sales mix, stronger service components and continued efficient cost management all made positive contributions to this end. In addition, the boom in Russia as a result of pull-forward effects due to expectations of the further devaluation of the Russian rouble had a positive impact during the Christmas season quarter.

Real

Sales at Real decreased by 8.3% to €7.7 billion in financial year 2014/15, as portions of the business in Eastern Europe sold in financial year 2013/14 had still contributed to sales. Real’s sales in Germany fell on a like-for-like basis by 0.8% in financial year 2014/15. Reported sales declined in particular as a result of store closings by 2.6% to €7.7 billion. In the fourth quarter of 2014/15, like-for-like sales at Real fell by 1.6%. Sales development at Real in financial year 2014/15 was especially impaired as a result of the competitive environment in the food sector, which remains quite fierce. The stores that have been remodelled in line with the successful Essen model, now numbering 107 locations, made positive contributions to the development of sales and customer frequency.

Real’s EBIT totalled €í441 million in financial year 2014/15 (2013/14: €19 million). This included special items of €529 million, related primarily to non-cash goodwill amortisation and store closings. EBIT before special items rose from €81 million in the previous year to €88 million.

Discontinued operations (Galeria Kaufhof)

At the heart of discontinued operations are Galeria Kaufhof and related consolidation effects. In financial year 2014/15, sales declined by 2.5% to €3.0 billion. In like-for-like terms, sales were down 1.9%. This development was due especially to the declining textile market. EBIT of €1,015 million included gains from the sale of Galeria Kaufhof amounting to €841 million and therefore cannot be compared with the previous year. As a result, EBIT before special items from discontinued operations totalled €175 million (2013/14: €196 million).

Additional information on the business development of METRO GROUP and its sales lines can be found in the Annual Report 2014/15 available at reports.metrogroup.de

2014/15 business figures

Q4 2014/15 business figures

METRO GROUP is one of the most important international retailing companies. It generated sales of some €59 billion in financial year 2014/15. The company operates at more than 2,000 locations in 30 countries and employs some 230,000 people. The performance of METRO GROUP is based on the strength of its sales brands, which act independently on the market: METRO/MAKRO Cash & Carry, the international leader in the self-service wholesale trade; Media Markt and Saturn, the European market leader in consumer electronics retailing; and Real hypermarkets.

More information is available at www.metrogroup.de

¹With the signing of the sales agreement concerning Galeria Kaufhof, Galeria Kaufhof has no longer been reported as a separate segment and part of the continued operations of METRO GROUP since the third quarter of 2014/15. It is reported instead as part of discontinued operations. METRO GROUP’s figures for financial year 2014/15 were adjusted for the Galeria Kaufhof figures, as were the previous year’s figures (with the exception of the balance sheet and the related information in the notes).

²Adjustment to the previous year’s figure due to discontinued operations (see notes to the consolidated financial statements in the Annual Report – notes to the group accounting principles and methods)

Source: metrogroup.de

By significantly reducing its net debt by €2.2 billion, METRO GROUP has further strengthened its balance sheet and thereby opened up room for making future investments. Plans call for raising the dividend of €0.90 per ordinary share in the previous financial year to €1.00 to include shareholders in METRO GROUP’s improved economic situation.

Thanks to the systematic implementation of their strategies, in addition to a number of measures and initiatives, the sales lines contributed to the successful development of METRO GROUP in financial year 2014/15.

METRO Cash & Carry focused even more towards the needs of its professional customers in financial year 2014/15 and succeeded in further expanding its delivery business, among other things. Sales from the delivery business rose by 13.7% to €3.1 billion (2013/14: €2.8 billion). Delivery sales accounted for 10.6% of METRO Cash & Carry’s total sales. Another milestone was the acquisition of Classic Fine Foods (CFF), one of the leading Asian providers in the high-growth food delivery business. Headquartered in Singapore, Classic Fine Foods directly supplies food to companies from the hotel, restaurant and catering (Horeca) segment.

METRO Cash & Carry also made important progress in terms of digitalsation. In order to be able to offer commercial customers of METRO Cash & Carry new services and technologies in future, METRO GROUP started the Techstars METRO Accelerator in financial year 2014/15. The support programme is being jointly implemented with US company Techstars, one of the most internationally renowned start-up networks, as well as the digital agency R/GA. The Techstars METRO Accelerator is geared towards founders with innovative technological applications for the Horeca segment. As part of the programme, experienced mentors and experts support selected start-up companies in successfully developing their own business within three months.

Since April 2015 METRO GROUP has also a stake in the US online job network Culinary Agents, a networking and job matching site for food, beverage and hospitality professionals. Due to the cooperation with METRO Cash & Carry this service is now offered in Italy and France since October for the first time.

In financial year 2014/15, Media-Saturn further accelerated its transformation from a primarily stationary provider of consumer electronics into a successful multi-channel retailer. The share of Media-Saturn sales generated online rose to more than 8%. The sales line is now represented by more than 1,000 stationary Media Markt and Saturn locations. With new formats such as Saturn Connect, which is a more compact city centre format focused on mobile communications, laptops, computers and other digital devices, Media-Saturn is also responding successfully to trends in traditional retailing. To further expand services for its customers, Media-Saturn acquired the majority stake in customer and repair service provider RTS in August 2015. RTS provides services for electronic products across Germany as well as through partners across Europe. The service range includes planning, installation, inspection, maintenance and repair for a wide variety of such products.

Real celebrated its 50th anniversary in financial year 2014/15. After hosting kick-off events at stores and central locations, the hypermarkets held discount campaigns and special promotional weeks dedicated to freshness, variety and innovation for their customers all year long. At the same time, the hypermarket operator continued to concentrate on enhancing the competitiveness of its locations and making them fit for the future. The locations that have been remodelled in keeping with the design of the Essen store are a key driver in these efforts. In financial year 2014/15, the successful concept was introduced at 57 additional Real stores. Real now operates 107 of these modern locations. Plans are being made to remodel more stores. Real also made progress with regard to a more competitive cost structure. A significant portion of product invoicing is now handled by Switzerland-based company Markant, which makes it possible to take advantage of standardisation and efficiency benefits.

Progress with portfolio optimisation successfully continued

METRO GROUP successfully continued to optimise its portfolio in financial year 2014/15. The most important transaction in this regard was the sale of Galeria Kaufhof¹, concluded on 30 September 2015. The purchase price was €2.825 billion, including various liabilities. The net cash inflow of €1.75 billion and the book profit of €0.8 billion exceeded the original forecast.

Additional measures aimed at focusing the portfolio in financial year 2014/15 were the sale of the wholesale business in Denmark as well as the disposal of the wholesale business in Greece. All of the documents necessary for the approval of the sale of the wholesale business in Vietnam have been submitted.

Business development 2014/15

METRO GROUP sales rose by 1.5% on a like-for-like basis in financial year 2014/15. Sales in local currency grew by 0.5%. However, the reported sales of €59.2 billion were down on the previous year’s figure by 1.2% due to negative exchange rate and portfolio effects. In Germany, like-for-like sales were on par with the previous year. At €22.5 billion, sales were down slightly overall on the previous year by 0.3%. This development was the result of a decline in sales at METRO Cash & Carry and Real. In the case of Real, store closings had a negative impact on sales. In contrast, Media-Saturn sales increased.

At €711 million, METRO GROUP’s EBIT fell short of the previous year’s level by €366 million in financial year 2014/15 (2013/14: €1,077 million). However, this figure included special items of €800 million (2013/14: €454 million). These special items can be divided into goodwill impairment losses (especially with respect to Real Germany at €446 million), restructuring and efficiency enhancement measures totalling €285 million (primarily planned closings) and other special items of €66 million. In addition, there was a positive special item from portfolio measures that totalled €23 million. Discontinued operations also contributed a positive special item of €841 million, which resulted from the proceeds of selling Galeria Kaufhof. METRO GROUP’s EBIT before special items decreased from €1,531 million to €1,511 million in financial year 2014/15. It should be noted, however, that negative exchange rate effects amounting to €117 million strained earnings. EBIT before special items thus rose considerably when measured in local currency.

METRO GROUP’s profit or loss for the period amounted to €714 million in financial year 2014/15, which is €532 million higher than the previous year’s level (2013/14: €182 million). Net of non-controlling interests, profit or loss for the period attributable to the shareholders of METRO AG amounted to €672 million (2013/14: €127 million). This corresponds to a significant improvement of €545 million. Profit or loss for the period included special items of €í26 million (2013/14: €491 million). Adjusted for these special items, profit or loss for the period amounted to €688 million (2013/14: €673 million).

In financial year 2014/2015, METRO GROUP generated improved earnings per share of €2.06 (2013/14: €0.39). EPS before special items amounted to €1.91 (2013/14: €1.84). This result provides the basis of the dividend proposal. On 25 November 2015, METRO AG already announced a change to its dividend policy. Due to METRO GROUP’s improved economic situation, plans call for raising the distribution ratio from the current range of around 40 to 50% to around 45 to 55%. The Management Board therefore intends to propose at the Annual General Meeting distributing a dividend of €1.00 per METRO ordinary share and €1.06 per METRO preference share for financial year 2014/15. This would correspond to a ratio of 52.4%.

METRO GROUP succeeded in considerably reducing its net debt year on year by €2.2 billion. Net debt totalled €2.5 billion as at 30 September 2015 (30 September 2014: €4.7 billion).

Outlook

The METRO GROUP forecast is based on the current group structure and refers to currency-adjusted figures. In addition, it is based on the assumption of a persistently complex geopolitical environment.

For financial year 2015/16, METRO GROUP expects to see a slight rise in overall sales, despite the continuously challenging economic environment. In like-for-like sales, METRO GROUP foresees another slight increase that will follow the reporting year’s rise of 1.5%. The sales lines METRO Cash & Carry and Media-Saturn in particular are expected to contribute to both total sales and like-for-like sales growth; we expect the Real sales line to improve its performance compared with the past financial year.

In financial year 2015/16, earnings development will also be shaped by the persistently challenging economic environment. Nevertheless, METRO GROUP is confident that it can again achieve an earnings increase as a result of the progress it has made and will continue to make in transforming its business models. Aside from operational improvements, METRO GROUP will again closely focus on efficient structures and strict cost management in this context in financial year 2015/16. For these reasons, we expect EBIT before special items to rise slightly above the €1,511 million achieved in financial year 2014/15, including income from real estate sales. METRO Cash & Carry and Media-Saturn in particular are expected to contribute to this development, while the development of the Real sales line will depend on the successful implementation of the measures that have been initiated.

METRO Cash & Carry

METRO Cash & Carry’s sales rose on a like-for-like basis by 0.9% in financial year 2014/15. In the process, it was possible to increase sales in every quarter. The previous year’s figure was matched in terms of sales in local currencies. Reported sales fell by 2.7% to €29.7 billion due to the development of exchange rates í primarily that of the Russian rouble í and portfolio effects.

METRO Cash & Carry’s like-for-like sales continued to see very positive development in the fourth quarter of 2014/15, growing by 1.1%. This marks the ninth consecutive quarter of such growth. Negative exchange rate effects and store disposals caused reported sales to decrease by 3.2% to €7.4 billion. However, sales in local currency were on par with the same quarter in the previous year.

METRO Cash & Carry’s EBIT totalled €975 million in financial year 2014/15 (2013/14: €904 million) and included special items of €75 million (2013/14: €221 million) In particular, these items consisted of restructuring and efficiency enhancement measures, among others, at METRO Cash & Carry Germany. EBIT before special items amounted to €1,050 million (2013/14: €1,125 million). This decrease is due especially to negative exchange rate effects in Russia. Adjusted for these effects, earnings before special items improved.

Media-Saturn

Media-Saturn’s sales rose on a like-for-like basis by 3.1% in financial year 2014/15. In the process, it was possible to increase sales on a like-for-like basis in every quarter of the financial year. Sales in local currency rose by 4.6%, and reported sales grew by 3.6% to €21.7 billion. Like-for-like sales at Media-Saturn improved by 2.9% in the fourth quarter of 2014/15, making it the fifth consecutive quarter of such growth. Reported sales increased by 2.9% to €5.1 billion (in local currency: +4.5%).

Online retail continued to see very dynamic development. Sales generated online rose by more than 20% and amounted to €1.8 billion. Online sales now account for more than 8% of Media-Saturn’s overall sales.

In Germany, like-for-like sales rose by 1.6%. Reported sales grew by 2.3% to €10.0 billion. The trend over the course of the year was extremely positive and was only dampend in summer due to a high level the previous year as a result of the FIFA World Cup. The further integration of the sales channels went over very well with customers. The pickup rate of goods purchased online was around 40%. The product range online was further expanded and at the end of September 2015 comprised more than 150,000 products at mediamarkt.de and some 130,000 products at saturn.de. As a result, the selection online now considerably exceeds the range offered at most Media-Saturn locations.

EBIT at Media-Saturn improved considerably to €336 million (2013/14: €244 million), which included special items of €107 million. These items consisted of numerous restructuring and efficiency enhancement measures. EBIT before special items rose appreciably from €335 million to €442 million. A better sales mix, stronger service components and continued efficient cost management all made positive contributions to this end. In addition, the boom in Russia as a result of pull-forward effects due to expectations of the further devaluation of the Russian rouble had a positive impact during the Christmas season quarter.

Real

Sales at Real decreased by 8.3% to €7.7 billion in financial year 2014/15, as portions of the business in Eastern Europe sold in financial year 2013/14 had still contributed to sales. Real’s sales in Germany fell on a like-for-like basis by 0.8% in financial year 2014/15. Reported sales declined in particular as a result of store closings by 2.6% to €7.7 billion. In the fourth quarter of 2014/15, like-for-like sales at Real fell by 1.6%. Sales development at Real in financial year 2014/15 was especially impaired as a result of the competitive environment in the food sector, which remains quite fierce. The stores that have been remodelled in line with the successful Essen model, now numbering 107 locations, made positive contributions to the development of sales and customer frequency.

Real’s EBIT totalled €í441 million in financial year 2014/15 (2013/14: €19 million). This included special items of €529 million, related primarily to non-cash goodwill amortisation and store closings. EBIT before special items rose from €81 million in the previous year to €88 million.

Discontinued operations (Galeria Kaufhof)

At the heart of discontinued operations are Galeria Kaufhof and related consolidation effects. In financial year 2014/15, sales declined by 2.5% to €3.0 billion. In like-for-like terms, sales were down 1.9%. This development was due especially to the declining textile market. EBIT of €1,015 million included gains from the sale of Galeria Kaufhof amounting to €841 million and therefore cannot be compared with the previous year. As a result, EBIT before special items from discontinued operations totalled €175 million (2013/14: €196 million).

Additional information on the business development of METRO GROUP and its sales lines can be found in the Annual Report 2014/15 available at reports.metrogroup.de

2014/15 business figures

Q4 2014/15 business figures

METRO GROUP is one of the most important international retailing companies. It generated sales of some €59 billion in financial year 2014/15. The company operates at more than 2,000 locations in 30 countries and employs some 230,000 people. The performance of METRO GROUP is based on the strength of its sales brands, which act independently on the market: METRO/MAKRO Cash & Carry, the international leader in the self-service wholesale trade; Media Markt and Saturn, the European market leader in consumer electronics retailing; and Real hypermarkets.

More information is available at www.metrogroup.de

¹With the signing of the sales agreement concerning Galeria Kaufhof, Galeria Kaufhof has no longer been reported as a separate segment and part of the continued operations of METRO GROUP since the third quarter of 2014/15. It is reported instead as part of discontinued operations. METRO GROUP’s figures for financial year 2014/15 were adjusted for the Galeria Kaufhof figures, as were the previous year’s figures (with the exception of the balance sheet and the related information in the notes).

²Adjustment to the previous year’s figure due to discontinued operations (see notes to the consolidated financial statements in the Annual Report – notes to the group accounting principles and methods)

Source: metrogroup.de